What Is an Attorney Trust Account?

Written by

|

March 6, 2024

Written by Smokeball

|

March 6, 2024

Written by Jordan Turk

|

March 6, 2024

Attorney trust accounts are critical to ensuring that money given to lawyers by clients or third parties is kept safe and not comingled with law firm funds or misused. But most people (even some new lawyers) must fully understand attorney trust accounts.

What is an attorney trust account?

An attorney trust account is a particular bank account where client funds are kept safe until it is time to withdraw them. Whether referred to as a client funds account or a lawyer trust account, using an attorney trust account is good business sense for lawyers holding money such as a retainer (or any other money) on behalf of a client for their case. And there are lawyer trust accounting guidelines that every attorney must understand and follow.

Separate client funds account

Every law firm has a fiduciary duty to separate client money from law firm funds. For example, a lawyer can only take a client's retainer to cover operating costs if the money has already been earned. The attorney trust account ensures the separation and security of client funds and helps law firms avoid accidentally commingling client funds with law firm funds. Generally speaking, there are two guidelines law firms should abide by:

- Maintain a single account to hold all client funds separate from the law firm's operating money. The lawyer is responsible for keeping up with the client's trust account and ensuring that funds are properly handled and that the status of each client's funds is tracked, OR

- Keep individual trust bank accounts for each client so that one client's funds aren't commingled with another's. Whichever guideline the lawyer follows, it's important to remember that an attorney can only spend a client's funds or retainer after the money has been earned. There are very few exceptions to this general rule.

While some lawyers may assume that keeping all client funds in a single client trust account is the method with the least amount of administrative work, it is a tactic than can create the most errors. Keeping track of how much of the money belongs to each client may take time to track. Fortunately, legal billing software solutions such as Smokeball provide trust account accounting so that there's never any doubt about how much money a client has in their trust account.

Earning an advance fee

A lawyer can earn a fee advance in some jurisdictions, but every jurisdiction has different rules. In some jurisdictions, depositing client funds into an attorney trust account isn't required. In others, lawyers can deposit funds directly into the law firm's operating account if the legal team has already earned the funds. But the rules around what money can be comingled or kept can get complex, so if there is any doubt about where the client funds should go, putting them into an attorney trust account is the wisest decision.

Interest on lawyer trust accounts (IOLTA)

IOLTA trust account definition: IOLTAs are a method of raising money to fund civil legal services for indigent clients through the use of interest earned on lawyer trust accounts.

In the United States, lawyers can place client funds in interest-bearing lawyer trust accounts. The Interest on Lawyer Trust Accounts (IOLTA) program was established in the U.S. in the 1980s. All 50 states and the District of Columbia have IOLTA programs. While all states have an IOLTA program, only 44 states require lawyers to participate. In states with mandatory IOLTA participants, the lawyer must place client funds into an attorney trust account and can only withdraw the money once they have earned the fee.

Smokeball legal billing software supports IOLTA trust accounts, but attorneys must pay close attention to the rules governing the jurisdiction in which they're working. Beyond the basic rule of depositing client funds into an attorney trust account in mandatory states, the rules can vary wildly from one jurisdiction to another. For example, some jurisdictions may require lawyers to place into an attorney trust account any portion of a flat fee that has yet to be earned.

Legal cloud practice management software

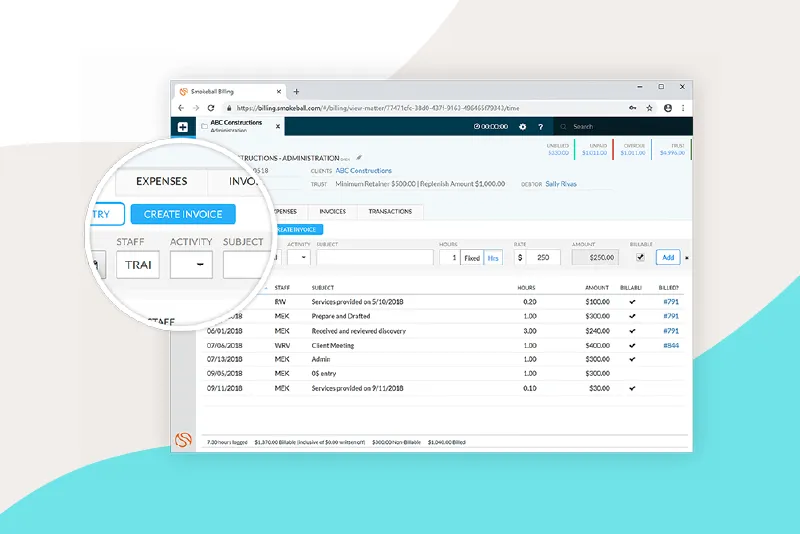

Managing lawyer trust accounts can become administratively burdensome if done manually and if there are a lot of clients to manage. This burden is why legal case management software such as Smokeball billing was designed to do the heavy lifting while keeping the lawyer compliant with the rules. Smokeball can provide the trust account balance on any client within minutes, no matter how many client funds the law firm manages accounts. There are also law firm insights reports and attorney time tracking software, making it easy to accurately bill for attorney work on the case and provide certifiable proof when a client inquires about the status of their money and how it is being managed. If you're looking for attorney billing and law practice management software in one solution, see a quick demo of Smokeball and see what it can do for your firm.

Avoiding trouble

There are a lot of rules around lawyer trust accounts. To avoid trouble and remain in compliance, law firms and lawyers should consider these best practices:

- Understand the consequences. When reviewing the rules, law firms must remain aware of the consequences of falling out of compliance with lawyer trust account rules.

- Remain transparent. Don't allow billing practices to become a mystery. Lawyers should leverage legal industry-specific software like Smokeball to track time and expenses accurately.

- Educate clients. Help clients understand what an attorney trust account is and what their rights are. The less ignorance around how a client's retainer or other funds are handled, the fewer billing complaints a law firm will experience.

- Never comingle funds. Always keep law firm operating accounts separate from client funds accounts so that there is never any appearance of noncompliance with the rules. The easiest way to achieve this goal is with trust accounts integrated into case management software.

For solo lawyers, clients, and law firms of all sizes, understanding how client funds should be handled is integral to maintaining transparency and trust. While getting a solid grasp of how lawyer trust account rules work is demanding, law firms must attempt to help clients understand so that billing conflicts are avoided on the backend.

Ready to see what Smokeball can do for your firm? Get your free demo today and see the Smokeball difference!

Trust Yourself With Trust Accounting

Watch on-demandRelated Product Content

Learn more about Smokeball document management for law firms:

Book Your Free Demo

Ready to see how Smokeball client intake software helps you Run Your Best Firm? Schedule your free demo!

Smokeball